Proud to be Powered by Vontier. Sharing a united vision that is driven by innovation. Find out more

Just before Christmas, the “Protecting Americans from Tax Hikes Act of 2015" legislation was ratified. A significant part of this modification to the tax rules is a permanent modification to Section 179 of the tax code, allowing purchasers of a capital equipment for small businesses to accelerate the depreciation of these improvements into the year of purchase.

This is a true “small business” incentive, potentially available to c-store owners, fuel marketers and other businesses with annual capital spending of up to $2.5 million. There are two parts to the provision:

- Same year deduction of up to $500,000. For capital spending of up to $500,000 on either new or used equipment, 100% of the investment may be deducted in the current year.

- “Bonus” depreciation. For spending on new equipment between $500,000 and $2 million, 50% of the capital spend can be deducted in the current year. For spending between $2 million and $2.5 million, the amount of the bonus depreciation is reduced proportionately.

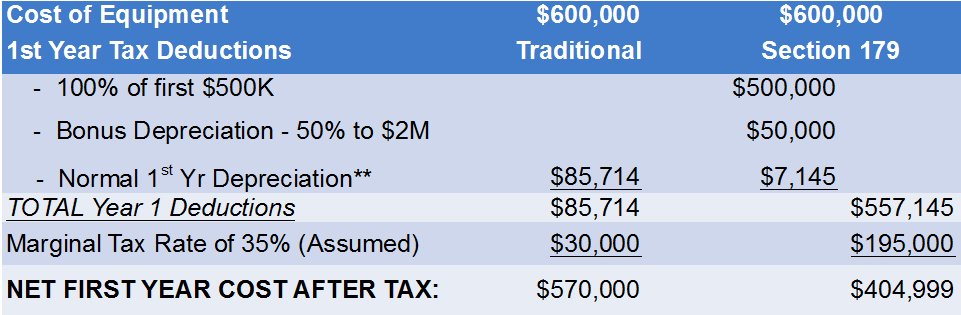

Here’s a scenario of how Section 179 could work to generate tax savings for a typical fuel marketer or convenience store:

With $600,000 of eligible capital equipment purchases in a year, a business may usually depreciate these assets over five to seven years. This would result in a tax deduction of $85,714 ($600,000 / 7 years). With Section 179, the business can fully deduct the first $500,000, plus 50 percent of the next $100,000. This $550,000 deduction leaves the book value of the asset at $50,000 ($600,000 - $500,000 - $50,000). This $50,000 can then be deducted over the seven-year asset life, providing an additional $7,145 deduction.

These deductions total $557,145, providing $195,000 is tax savings in the first year. Capturing 93% of the available depreciation in the first year is a strong incentive to accelerate the purchase of new equipment, including EMV upgrades. This can be of high value, especially in an environment where technicians may be in short supply during the EMV upgrade cycle.

The types of improvements that can be deducted under the enhanced Section 179 code include:

- EMV equipment upgrades, including EMV pumps, EMV retrofit kits and point of sale upgrades

- In store equipment such as beer caves or fixtures

- Energy efficiency improvements, including LED lighting and HVAC equipment.

- Underground storage tank compliance work to meet the updated EPA UST regulations

- If you lease, rather than own, your building, you can even deduct limited structural changes – things like interior walls and doors – under the new Section 179 provisions.

We recommend that you review your specific situation with your accountant or financial advisor prior to developing your purchasing strategy. Combining use of available tax incentives with equipment financing and other manufacturers incentives can potentially enhance your cash flow and operating margins.